Written Commentary

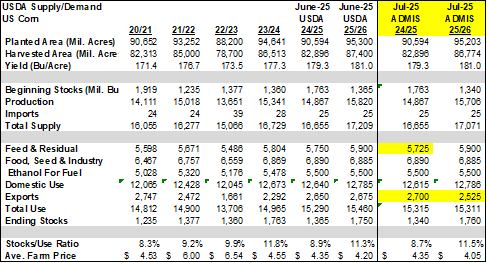

Prices were $.05-$.07 lower today as most contracts scored new contract lows while Sept-25 closed under $4.00 bu. Spreads were little changed. Crop ratings improved 1% to 74% G/E. Overall ratings are the highest since 2016. 18% of the crop is silking, below the 22% from YA however just above the 5-year Ave. of 15%. Money managers sold just over 24k contracts in the week ended Tues. July 1st extending their short position to just over 206k, the largest since Aug-24. The USDA reported the sale of 113k mt (4.5 mil. bu.) to Mexico for the 25/26 MY. Brazil’s 2nd crop harvest remains a slow go due to delayed plantings, high moisture levels combined with the sheer size of the crop.

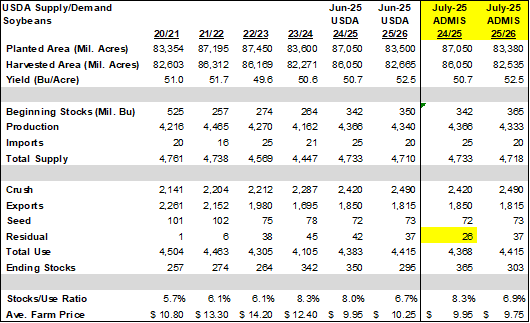

Prices were lower across the complex. Beans were off $.03-$.10 with old crop futures making new lows late. Meal was down $1-$2 while oil was 10-20 higher. Bean and oil spreads were stronger while meal was mixed. Both old and new crop bean futures held just above recent lows. Support for Aug-25 is at $10.16 ¾, and $10.13 ¼ for Nov-25. New contracts low for Aug-25 meal. Inside trade for Aug-25 oil as it consolidates near $.54 lbs. The USDA did announce the sale of 144k mt of meal to the Philippines. Spot board crush margins (Aug-25) closed at $1.69 ½ bu. with bean oil PV settling right at 50%. New crop crush margins improved $.01 ½ bu. to $4.02. Trade tensions combined with crop friendly weather continue to weigh on commodity valuations. Non-threatening US weather continues to drive record yield expectations for both US corn and soybean crops. After sending out roughly a dozen letters yesterday to trading partners spelling out what each countries reciprocal tariffs will jump to on Aug. 1st, Pres. Trump today stated this date will not change. Soybean ratings held at 66% G/E however there was a 1% shift from good to excellent. 32% of the crop is blooming with 8% of the crop setting pods, in line with the historical average. In the most recent reporting period MM’s were net sellers of 23k soybeans, 5k oil and nearly 22k meal. Their record short position in meal extended to 132k contracts. EU bean imports for 24/25 totaled 14.5 mmt, up from 13.2 mmt YA. Meal imports at 19.4 mmt were up from 15.3 mmt YA and above the USDA forecast of 18.8 mmt. Today USDA Sec. Rollins stated there will be no amnesty for agricultural workers in the Trump Administrations effort to deport all illegal immigrants.

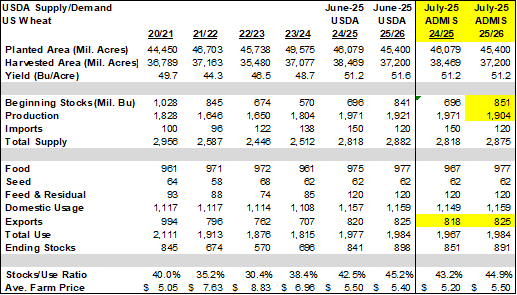

Prices ranged from steady to $.02 lower in CGO to $.05 lower in KC and MIAX futures. Spreads have firmed in CGO while weaker in KC. Winter wheat ratings held steady at 48% G/E vs. however there was a 2% shift from poor to fair. Likely the last ratings report of the year. Harvest advanced to 53% complete vs. YA pace of 62% and 5-year Ave. of 54%. Spring wheat conditions slipped 3% to 50% G/E, vs. expectations for no change. 61% of the crop is headed vs. 56% YA and the 5-year Ave. of 58%. MM’s were lite buyers in KC and CGO wheat while small sellers in MGEX futures. Their combined short position across the 3 classes has now fallen for 7 consecutive weeks to just under 107k contracts vs. 235k in late May. Shortly after Russia’s Ag. Ministry temporarily eliminated their wheat export tax, SovEcon raised their Russian 25/26 wheat export forecast 2.1 mmt to 42.9 mmt, still below the USDA est. of 45 mmt. My all wheat production forecast for Fri. is 1.904 bil., down 17 mil. from June-25

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.